Lazy Metrics¶

spark-bestfit supports lazy metric evaluation with true on-demand computation. KS/AD metrics are computed only when you actually need them, providing significant performance improvements for model selection workflows.

Metric Computation Cost¶

Not all goodness-of-fit metrics have the same computational cost:

Metric |

Cost |

Notes |

|---|---|---|

SSE |

Fast (~ms) |

PDF evaluation at histogram bins |

AIC / BIC |

Fast (~ms) |

Log-likelihood sum |

KS-statistic |

Moderate (~100ms) |

O(n log n) sort + CDF computation |

AD-statistic |

Slow (~200-500ms) |

O(n log n) sort + 2n log operations |

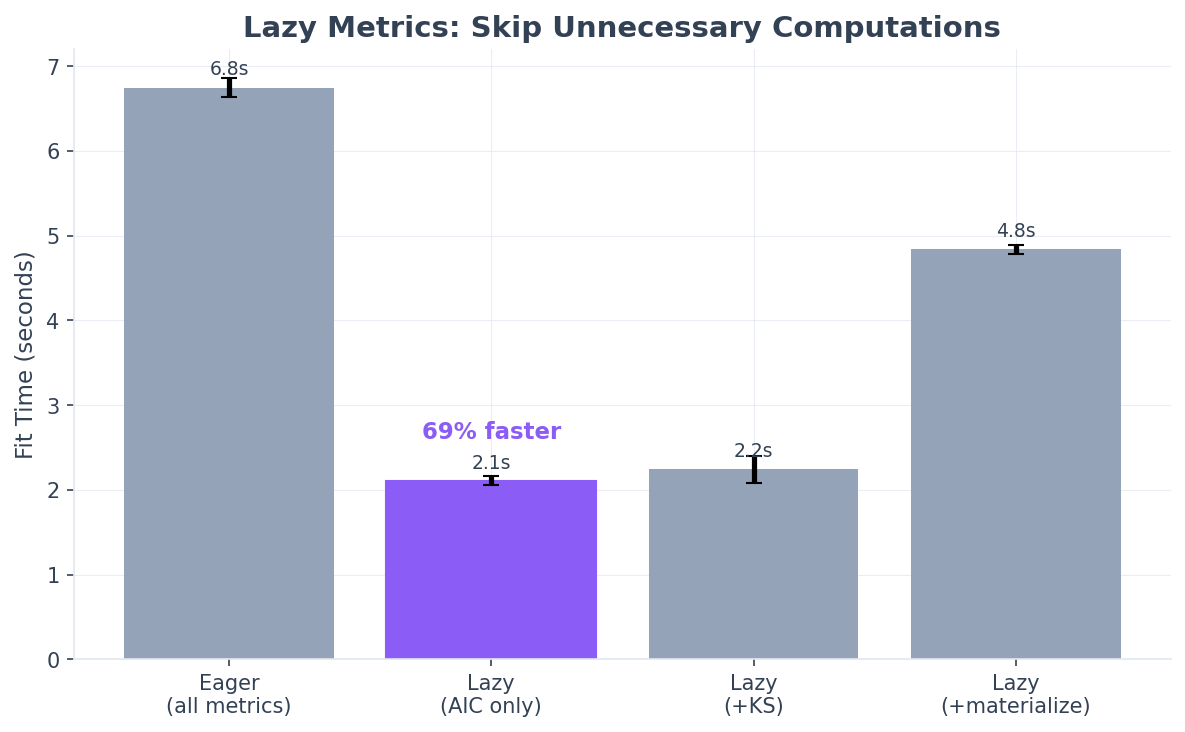

With ~90 distributions (default), computing KS/AD for all can add 20-50 seconds to the total fitting time. With lazy metrics, you only pay this cost for the distributions you actually access.

Using Lazy Metrics¶

Enable lazy metrics to skip initial KS/AD computation during fitting:

Using FitterConfig (v2.2+, recommended):

from spark_bestfit import DistributionFitter, FitterConfigBuilder

fitter = DistributionFitter(spark)

# Build config with lazy metrics

config = FitterConfigBuilder().with_lazy_metrics().build()

# Fast fitting: skip KS/AD computation initially

results = fitter.fit(df, "value", config=config)

# Check if results are lazy

print(results.is_lazy) # True

# Get best by AIC - fast, no KS/AD needed

best_aic = results.best(n=1, metric="aic")[0]

print(best_aic.ks_statistic) # None (not computed yet)

# Get best by KS - triggers ON-DEMAND computation!

best_ks = results.best(n=1, metric="ks_statistic")[0]

print(best_ks.ks_statistic) # 0.0234 (computed value!)

Using parameter directly:

# Alternatively, pass lazy_metrics parameter directly

results = fitter.fit(df, "value", lazy_metrics=True)

Key insight: When you call best(metric="ks_statistic") with lazy results,

spark-bestfit automatically:

Gets top N*3 candidates sorted by AIC (fast, already computed)

Computes KS/AD only for those candidates (not all ~90 distributions)

Re-sorts by actual KS and returns top N

This means you get correct results while computing metrics for only ~5% of distributions.

Materializing All Metrics¶

If you need all metrics computed (e.g., before unpersisting the source DataFrame),

use the materialize() method:

# Fit with lazy metrics

results = fitter.fit(df, "value", lazy_metrics=True)

# Fast model selection

best_aic = results.best(n=1, metric="aic")[0]

# Before unpersisting, materialize all metrics

materialized = results.materialize()

print(materialized.is_lazy) # False

# Now safe to unpersist source data

df.unpersist()

# Access any metric on materialized results

best_ks = materialized.best(n=1, metric="ks_statistic")[0]

print(best_ks.ks_statistic) # Computed value

Warning

If you try to compute lazy metrics after the source DataFrame has been

unpersisted, you’ll get a RuntimeError. Always call materialize()

before unpersisting if you need KS/AD metrics later.

When to Use Lazy Metrics¶

Use lazy_metrics=True when:

You’re doing model selection using AIC/BIC (recommended for most cases)

You’re iterating quickly and want faster feedback

You only need KS/AD for a few top candidates

You’re fitting many distributions and want faster iteration

Use lazy_metrics=False (default) when:

You need KS/AD statistics for all distributions upfront

You want to filter results by KS thresholds (

filter(ks_threshold=0.1))You need p-values for statistical significance testing on all fits

You plan to serialize results and need complete data

Filter Behavior¶

Note that filter(ks_threshold=...) cannot trigger lazy computation because

it needs to evaluate all rows. If you use filtering with lazy results, a warning

is emitted:

# This will warn - can't lazily compute for filter

filtered = results.filter(ks_threshold=0.1)

# Instead, materialize first, then filter

materialized = results.materialize()

filtered = materialized.filter(ks_threshold=0.1)

Why Lazy Metrics Matters¶

The value of lazy metrics isn’t measured in wall-clock speedup for a single fit - it’s about skipping work you don’t need across your entire workflow.

The core insight: When fitting ~90 distributions (default), you typically only examine the top 3-5 results. With eager evaluation, you compute KS/AD statistics for all 90 distributions. With lazy evaluation, you compute them for only the ones you actually access.

Workflow |

Eager Mode |

Lazy Mode |

|---|---|---|

|

90 KS/AD computations |

0 KS/AD computations |

|

90 KS/AD computations |

~5 KS/AD computations |

|

90 KS/AD computations |

90 KS/AD computations |

Scaling Characteristics¶

Why lazy metrics scales well for production workloads:

Fixed sample size: KS/AD computation uses a fixed 10K sample regardless of data size. The savings are constant whether you have 100K rows or 1 billion rows.

Multiplicative savings: When fitting multiple columns or running repeated experiments, the savings multiply:

10 columns x 5 iterations x 85 skipped distributions = 4,250 KS/AD computations avoided

Interactive workflows: During exploratory analysis, you iterate quickly using AIC/BIC for model selection. Lazy metrics gives you instant feedback without waiting for KS/AD computation you won’t use until final validation.

Surgical on-demand computation: When you request

best(metric="ks_statistic"), we get top candidates by AIC first (already computed), then compute KS/AD for only those ~5 candidates - not all 90 distributions.

Production recommendation: Use lazy_metrics=True as the default for

exploratory analysis and model selection. Only use lazy_metrics=False when you

need KS/AD statistics for all distributions upfront (e.g., for comprehensive reports

or filtering by KS threshold).